AH090 - The Survey Says: Inflation is a Problem, and Change is Imminent, with Business Group on Health's Jim Winkler

.webp)

For Episode 90 of Astonishing Healthcare, Jim Winkler, Chief Strategy Officer at Business Group on Health, joins us in the studio for a lively discussion about the results of their 2026 Employer Health Care Strategy Survey! This annual study is packed with qualitative and quantitative information and highlights the top trends in employer-sponsored health care. Jim brings decades of experience to the table and puts helpful context around the headline data and employers' expectation for a ~9% year-over-year health care cost increase. He also shares his perspective on the evolution of the role benefits brokers and consultants play, how employers can navigate the rapidly evolving market and inflationary storm, vendor accountability, and how to position difficult decisions around making big changes.

Discussion Highlights

- Costs are expected to rise 9% in 2026, marking the worst multi-year surge in over a decade - the volatility is a real issue, as it’s another year of healthcare costs rising by more than benefits teams forecasted.

- Pharmacy's share of the total cost has jumped to 24%, driven by expensive GLP-1 and cancer drugs, and some other new cost drivers include mental health and autoimmune conditions.

- Proactive employers have been reviewing their data and are optimizing their programs, cutting underused solutions, investing where there’s a tangible return, and tightening controls on high-cost treatments.

- Employers are aggressively scrutinizing partners and exploring alternative PBM and health plan models, as they should be (vendor accountability has become increasingly important over the years) - change is imminent (i.e., expect an acceleration of RFP activity).

Listen in below or on Apple, Spotify, or YouTube Music!

Transcript

Lightly edited for clarity.

[00:22] Justin Venneri: Hello and thank you for listening to another episode of Astonishing Healthcare. I'm Justin Venneri, Senior Director of Communications here at Judi Health, and Jim Winkler, Chief Strategy Officer at Business Group on Health, is in the studio with me today. I've also got to give a shout out before we get started to Brenna Shebel at your firm for helping coordinate this one and a shout out for all the great research and studies you all do that she coordinates and oversees. But thank you, Jim, for joining us today.

[00:44] Jim Winkler: Glad to be here and really appreciate you giving Brenna and her team a shout out. As you can imagine, this is a huge undertaking and they do amazing work.

[00:51] Justin Venneri: Absolutely. So why don't you start us off with a bit about your background and role at Business Group on Health.

[00:58] Jim Winkler: Sure. So I'm the Chief Strategy Officer for Business Group on Health. We are a collaboration or membership organization of employers and the industry partners that serve them like Capital Rx. Thank you for being a member company. Our job is to bring together employers and their partners to really think about, discuss, debate and operationalize best practices in health and wellbeing.

My role is to help the organization think through what comes next in healthcare. How do we take interesting insights like the survey data that we'll talk through today and really turn that into practical, how-to information for our members. I've been in the healthcare related industry for decades now instead of years because it's been so long. I spent most of my career as an employee benefits consultant, at Hewitt Associates and then AON after that, and joined the business group about three years ago.

[01:47] Justin Venneri: Okay. And I always wonder, all the regional Business Groups and Business Coalitions on Health out there, there's no affiliation, right? Everybody's separate?

[01:53] Jim Winkler: There's no affiliation. So we have a common naming mechanism that stems back to 50 plus years ago when our organization started, but we're completely independent of each other. Many of our employer members are members of relevant regional groups that make sense for their populations. We collaborate on public policy types of things most notably, but otherwise we are operationally independent.

[02:14] Justin Venneri: Cool. Okay. And your annual survey, the reason we're here, it's one of my favorite reads and is always packed with info. Can you provide listeners with a little context and the story behind it? What's the primary objective? Does that change? How's it designed? What are the demographics? I apologize, I do this a lot, ask a lot of questions in one.

[02:32] Jim Winkler: No worries. So we call it the Healthcare Strategy Survey. And that's intentional. There are a lot of surveys in our industry, many that get into tactical specifics—what's your average deductible or copay or things of that nature. And those are really, really important and employers benefit from those. We take a different approach. Ours is very much focused on what are the key things employers are thinking about as they head into the next year, in this case as they're heading into 2026. What are some of the drivers of that thought process, often rooted in what is happening as it relates to both healthcare costs and the conditions and experiences that are driving those costs.

So, this survey, we fielded it over the summer, June - July timeframe. 121 employers with about 11 and a half million lives around the world, including 7.4 million lives in the U.S. so it's a robust survey in terms of number of employers, but it's also employers that cover anywhere from a few thousand employees on up to a million employees. So a rather good indicative data set of what employers are thinking about as they deal with challenges in healthcare going forward.

[03:32] Justin Venneri: Got it. And high-level findings. The headline is or was obviously another year of escalating costs following two years of actual costs exceeding forecasts. What are you seeing, or what are the respondents telling you, and attributing what is basically unchecked inflation to?

[03:48] Jim Winkler: So let me just spend a minute or two on the actual cost numbers, because as I said, I've been doing this a long time. For years and years, you could take any snapshot of a survey like this over the last decade or two and you'll find that the height of the bars is always going up. Lots of people say healthcare costs are growing at an unsustainable rate. I annoy our team often by saying I've been doing this for 30 years. They've been growing at that level for 30 years. That's actually the definition of sustainability and that's actually the problem. The problem is that we're sort of numb to the actual cost to some extent.

But I think what makes this year's results interesting are a couple of factoids. One, as you pointed out, two years in a row, 2023, 2024, employers tell us that actual costs came in higher than forecast. And that's a sign of volatility. As bad as absolute healthcare costs being high can be for an organization, volatility is really a challenging thing for an HR professional to have to go to finance and say, “Hey, for the second year in a row, we got it wrong in the wrong direction.” It makes it really difficult for organizations to manage overall expense.

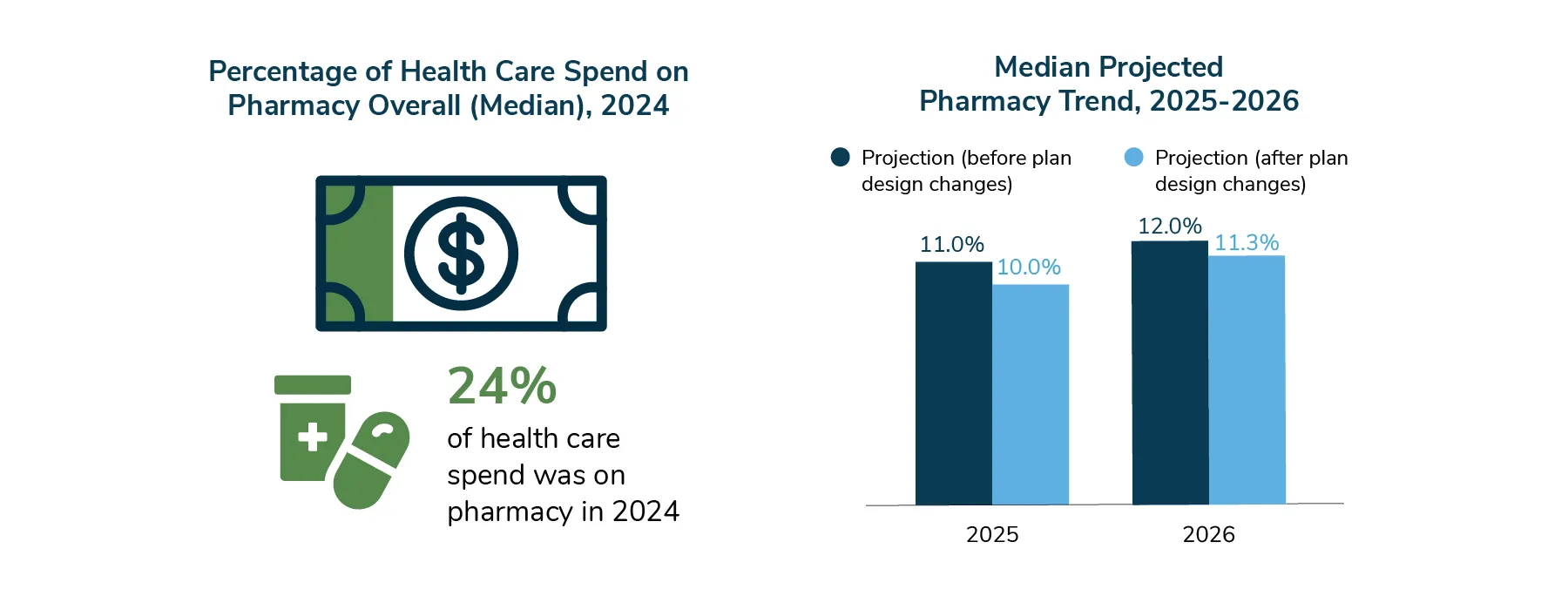

It also candidly calls into question their credibility. You think about mid-2025, which is when we did the survey, employers saying, yep, another year In a row, 2024, my actual costs exceeded my forecast. Difficult situation with finance. You're now halfway through 2025. At that point, chances are finance is not loving the credibility of your forecast for 2025. And for 2025, employers were telling us they were expecting an 8% increase, 6.8% after plan design changes. So a high number that we're probably going to exceed for the third year. That's certainly what I expect when we report these results next year.

And then 2026, employers basically said, hey, before they make plan changes, healthcare costs were expected to go up 9%, which is the largest single-year increase we've seen in more than a decade. You put all those pieces together—volatility, unpredictability, challenges with having to navigate your finance organization and booking a number that is really, really high—you start to take a step back and pause. When you look at 2023 to 2025 as a three-year block, it'll likely end up as the highest three-year rate of increase that we've seen since 2009 to 2011.

And in 2009-2011, we got things like the Affordable Care Act and a massive migration into high-deductible health plans. We saw a lot of vendor change and consolidation. We saw hospital consolidation. Big things happen when healthcare costs have that kind of multi-year uptick. We're really mindful of that as the underpinnings of everything. We'll talk about what employers are thinking about and what they're doing, rooted in this environment in which there is a mandate for change. Change will happen. It'll either happen strategically by employers making smart decisions about their plan and their strategy, or it will happen to them because the market will respond.

[06:45] Justin Venneri: Yeah, that makes a ton of sense to me. You kind of slipped and said interest there for a sec.

[06:49] Jim Winkler: It feels like that.

[06:50] Justin Venneri: Yeah. It's like compounding against you year-on-year, as if it's a high-interest credit card and it's just unbearable. Then that becomes a vicious debt cycle at some point, and you can't get out of it. I think it's gotten that serious.

So our audience and your audience, mostly people in and around the pharmacy benefits space and now health benefits as we've transitioned to Judi Health. Whether it's benefits brokers and consultants, plan sponsors, health plans, folks working in managed care or following managed care. I think everybody knows the pharmacy trend, what it's been, as you noted, overall volatility. But pharmacy spend rising faster than everything else. What are respondents saying and what are your thoughts about pharmacy spend as a percent of the total spend and the drivers?

[07:29] Jim Winkler: That's an interesting one. It honestly gets to the compounding we were talking about. Over the last three years, pharmacy as a percentage of the total has gone up from 21% to 24%. On balance, maybe that doesn't seem like a lot. But keep in mind what healthcare costs overall have done over that time period that we just talked about. The worst three years in well over a decade. It really means that pharmacy costs over that time period have increased by almost 40% because it's 24% of a much higher number now. So at its core, much of the volatility in healthcare that we're dealing with overall is rooted in pharmacy.

Pharmacy Cost Trends, 2024-2026

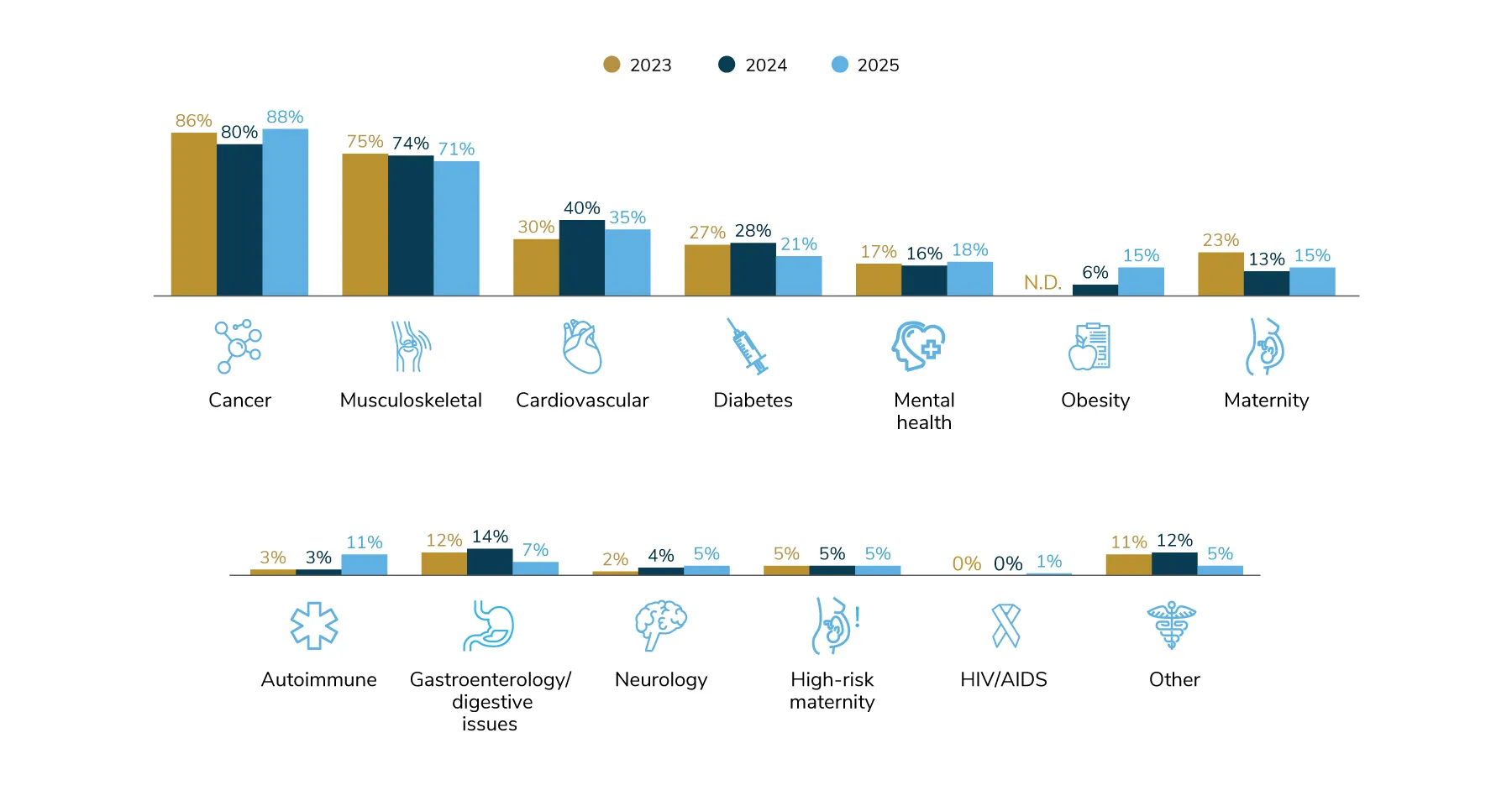

It's not just attributable to pharmacy, but it's rooted in pharmacy in that much of the cost on the pharmacy side is tied to things that are expensive on the medical side. So GLP-1s for diabetes, heart disease, obesity—those are conditions that, on the medical side, are expensive to deal with and are growing in prevalence and growing in cost. And we've got a pharmaceutical treatment that's adding significantly to that cost. The same is true for a condition like cancer. Cancer is the number one cost driver for employers. That's what, multiple years in a row, we're seeing that in the data, and the pharmacological treatments associated with that are growing in expense as well. So it's not like we have a pharmacy cost problem, but medical's running fine. We have a cost problem on both sides, and that's what makes it really volatile.

[08:44] Justin Venneri: Okay. And the report in total is 70-plus pages of data just packed, and the press release covered the key takeaways. We talked about the headline cost numbers. Can you share a little bit more what's behind the curtain and not widely published from this year's survey? Maybe just two or three data points that you found particularly interesting?

[09:00] Jim Winkler: This survey always gets widely published and this year in particular, because of what the cost numbers are, it did get very widely published. So I'm not sure that I could think of a really good data point that hasn't been talked about. But I would say there can be a tendency to just over-rotate on the absolute cost numbers and that volatility and kind of lose sight of some of the things that sit underneath that.

For example, while cancer showed up as the number one cost driver for the fourth year in a row, things like mental health jumped up. Mental health is one of the top five cost drivers now. If you think back to five or ten years ago, we would talk about a topic like mental health and we would say we have a foundational access issue in this country. People can't get care for mental health. The good news is we've done a lot to destigmatize mental health, and through a variety of both virtual and bricks-and-mortar solutions, we've increased access. That's awesome. But guess what? That care is not free. And so now we have a mental health cost dynamic that we have to navigate that has both medical and pharmacy applications to it. Now there's an opportunity for employers to start to think about, are people getting the appropriate care? Are they getting high quality care? Are they getting care at the right level in terms of coaching versus therapy versus psychiatric clinical care?

Another similar area that's very underreported in the data because its absolute number is low, but jumping up, is autoimmune. Autoimmune conditions went from being about 3% of employers saying it's a cost driver to about 11%.

Conditions Driving Costs, 2023-2025

Health Benefits Data & Other Related Content

- How employers can take back control of unnecessary pharmacy spending

- Replay - Strategic Well-Being: Rethinking Health Benefits to Empower Employees and Drive Impact

- Signs it is time to change your PBM vendor, and how to overcome common hesitations

- Health Benefits 101: The Importance of a Transparent PBM Model

[10:38] Jim Winkler: When we think about our top five, autoimmune comes in eighth. So on balance, you'd be like, hey, nothing to worry about. But the reality is it has jumped up. One reason why it has jumped up is because the treatments for autoimmune are expensive. It may not impact as many people in your population as cancer or cardiovascular or musculoskeletal, but the cost per patient is pretty significant. That's a category we're going to pay attention to. So those are some things that I would highlight that maybe are underappreciated in all the discussion of GLP-1s being expensive.

[11:12] Justin Venneri: Makes sense. One thing that jumped out at me. I'm wondering if you can comment on the vendor accountability piece of the puzzle here. Seemed like that became a bigger focus than I recall in past years.

[11:21] Jim Winkler: A colleague asked me if I thought that employers historically have not held their vendors accountable and if so, why. I said, well, I actually think they have held their vendors accountable. I think what we're talking about is a necessary ramping up in that regard. I think that's true across the board. In our survey we asked about things like alternative PBMs, alternative health plans. In our annual survey focused on wellbeing that we published a few months ago, we were asking questions about holding vendors accountable in the same way.

When you are in a situation like employers find themselves with healthcare costs being what they are, the overall experience for plan participants hasn't been stellar. We've thrown lots of vendor programs at employees, right? So many employers have 20, 30, 40, 50 vendors in their ecosystem. You start to look and say, all right, which of these are actually doing what they purport to do and are they doing it well for enough people for it to be worth my time? I'm going to have to really dive into managing my program more aggressively. So I think the employer message is we're going to be much more likely to scrutinize whether it's our consulting relationship, our health plan relationship, our PBM relationship, our point solution relationships to really focus on who's genuinely delivering value that aligns with my goals as an organization, not their own. And really pushing the market toward greater collaboration across vendors in service to the employer and being comfortable saying I'm going to turn things off that really are underperforming. It's taking accountability from an important fiduciary responsibility to that, plus I really have to focus on the partnerships that really drive success going forward.

[13:07] Justin Venneri: And you took the words out of my mouth. I was about to say, given the fiduciary obligations and CAA that everybody's been talking about for years, you kind of have to get into the nitty-gritty and start holding people accountable for what they're supposed to be delivering based on what you're paying them.

[13:21] Jim Winkler: Self-insured employers have a fiduciary responsibility under ERISA that is meaningful and material and something they all take very seriously. I think the standard for employers candidly is probably less about what do I need to do to be a good fiduciary under ERISA. I think it's, what am I doing to do my job well, to be a good steward of a program that is growing in expense, that isn't solving enough of the complex chronic conditions I need it to solve—cancer, musculoskeletal, diabetes, heart disease, et cetera—and increasingly is creating a subpar experience for my employees. At the end of the day, I want what I'm responsible for to work more effectively. So I'm focused on it from that perspective, not just because ERISA and laws that have followed that have created a fiduciary responsibility. It's going from that to the next level.

[14:13] Justin Venneri: I think this is probably a good spot for my curveball question, courtesy of Josh Golden. You mentioned earlier your experience at Hewitt. How do you think the consulting world has changed or evolved since your early days in benefits consulting?

[14:25] Jim Winkler: Really, really good question. The consulting industry has evolved in a couple of ways. For starters, the degree of difficulty associated with consulting to an employer is much higher now than it was 10 or 20 years ago. What employers have to tackle and what they need their consultant or their broker to help them with is much more complicated. It's not as straightforward as just taking the plan out to bid every couple of years. The average benefits consultant has to understand clinical things way more than we had to 10, 20 years ago, just to be conversant in topics like cell and gene therapy. It's harder to be a consultant from a knowledge-required standpoint.

And as those firms have grown and as employers have been really prudent about how they engage consultants, it's just harder to grow that business as a consulting firm. They have to think about different ways to serve their customers. I think in a space like pharmacy where you all play, as it's gotten more complex, the financial engine that sits behind the pharmacy business is way more complex today. Consultants have to keep up with that. They have to adapt their models to evaluating emerging solutions. You think about in the PBM world as new solutions come on the market. Take the direction of your organization as you move from just a PBM to a platform via Judi® How do I evaluate that? Does it fit into the financial model my firm has built to evaluate PBMs? How do I think about rebate-free models or transparent models versus traditional models? All of that is much more complicated.

[16:17] Justin Venneri: That's a timely comment too, given all the news recently about rebates. Kind of back to the survey and building on what you've been saying, can you highlight one or two of the themes or questions that resulted in a surprising year-over-year shift that you think everybody should key in on?

[16:33] Jim Winkler: We don't do a lot of year-over-year comparison in the survey. The results each year kind of tell their own story. But I think some things I would point to where we're seeing some movement are things like biosimilar coverage, for example. A year ago, about a third of employers basically said, "I actually don't know how biosimilars are managed in my program." This year that number was only 17%, which is still kind of high, candidly. Almost two out of 10 are telling us that they're not sure how biosimilars work in their plan. But that's much better than it was a year ago.

I think the other one that's interesting is when we asked about adoption of nontraditional or alternative programs. In the alternative PBM or new generation PBM space, 27% of employers said that they either have it in place or will in 2026. But another 43% are considering it for '27 or '28. A big percentage would suggest lots of RFP activity. And on the medical alternative health plan side, about 24% expect to have something in place in 2026. Another 36% are looking at it. So those numbers, I would expect a year from now we would see higher adoption. When you've got 43% of employers looking at alternative PBMs and 36% looking at alternative health plans, some big portion of those will adopt something.

[18:26] Justin Venneri: Definitely. And how about a practical action? An employer listening to today's podcast episode, what's something they could consider or something a consultant could suggest a client look at?

[18:36] Jim Winkler: Maybe a couple of things. One of the questions we ask in the survey is a hypothetical that basically says if your organization came to you and said you have to deliver next year's benefits plan at the exact same cost, so 0% trend against that 9% number we talked about, what would you do? The one area that employers basically said "I'll only go there as a last resort" is eliminating the current program and sending people into the individual market. At this point at least, the vast majority of employers, 87%, said they're not looking at that route.

But some of the things employers said they would consider are an RFP process to narrow my array of vendors and really drive toward high-performing vendors, eliminating lower-utilized programs. And then one that's really germane to your audience is limiting or reducing coverage for GLP-1s. At the time we did this survey, only about 7% of employers said "I'm going to drop GLP-1 coverage for obesity or for weight loss next year." I suspect if we were to run this survey today, you'd see a higher percentage. We've heard anecdotally more employers saying here's something I can do right now, and that is either eliminate the coverage completely or more aggressively tie the coverage to lifestyle modification programs that hopefully help a person who uses the medications lose weight, but then has to figure out how to live differently to not regain the weight.

Some of the things we've been talking about with employers that maybe go a little bit outside the survey would be things related to the employee experience. One aspect is streamlining your lineup of vendors. Make it more readily visible to employees where you want them to go for what. That might take the form for some employers of leaning into things like a navigation solution that allows you to say to your employees, "We offer a lot of different programs, start here always and they'll get you to the right place."

The other is many employers leaning into using AI to more effectively personalize employee communications around health and wellbeing, making it less benefits-speak and more common-person language. We're pretty good at explaining things at annual enrollment. But most of us don't choose to get sick the week after annual enrollment when we've read all the materials. It happens over the course of the year and you don't remember what new program is offered or what number to call. AI can help make that much more simplified and much more straightforward.

[21:47] Justin Venneri: That's a good one. I just wrote Samantha Custer who's been on the show before with me doing a transition benefits episode (Episode 39). More about open enrollment and tips employers can leverage to try to make that more of a year-round educational thing versus an open enrollment thing and have people be more aware of the benefits they have. That's a really good one. Thank you so much, Jim for taking the time with us today.

[22:11] Justin Venneri: Before I get to the last question, where can people find you or more information on Business Group on Health?

[22:20] Jim Winkler: Our website is a great treasure trove of information. The website address is www.businessgrouphealth.org, all one word. Tons of information there. Much of it is inside the firewall, gated for our member organizations. But one of the member benefits is access to a ton of great thought leadership ranging from innovative, strategic thinking to practical, tactical, how-to materials. We do have a decent amount of information, including the executive summary for this survey and all of our surveys, that's in the public domain. And there's information on our website about how to become a member. You mentioned our annual conference. It takes place in April every year. It'll be in New Orleans in April of 2026. Registration for that will open in December. It's open to any employer. They don't have to be a Business Group member to attend our annual conference. For industry partner organizations like Capital Rx, you do have to be a member.

Additional Business Group on Health Links/Resources

- 2025 Employer Well-being Strategy Survey: Executive Summary

- Business Group on Health - Resources (Surveys, Data, etc.)

[23:24] Justin Venneri: Understood. All right, last one. What's the most astonishing thing you saw in this year's survey or relating to this discussion today? What's the biggest eye-opener?

[23:45] Jim Winkler: Excellent question. Probably the biggest aha is when you put all those little heights of the bars on the cost chart together and paint that picture of missing forecast two years in a row, three years that look as bad as it's been since 2009 to 2011, and then talking about what happened in the marketplace then. For many benefits professionals, whether those are consultants or people in benefits roles at employers, they weren't in those roles in 2009-2011. This feels different. The key message and the key conversation, and where you really get that aha, is this is different than a 5 or 6% trend year you might have had a couple of years ago.

That leads us to this notion of being fearful of change because change is disruptive. That has generally been a challenge in our industry. Employers will look at new solutions and think "This will be really hard to implement. This is disruptive to my people." And the reality is, when you look at where we are in the US today, we're asking people to pay out of pocket somewhere in the neighborhood of five to six thousand dollars for a system that we can tell from the clinical results isn't treating them effectively enough. Cancer, chronic conditions, all those things are on the rise, and people are consistently having a crappy experience. So why are we trying to protect that system and be fearful of disrupting it? We actually should lean into it and say to our employees, "Good news, we're going to do something different. I know that different can mean change, and that can be scary, but we're moving away from this thing that isn't working for you or for us." Those kinds of conversations, which the survey data starts to point you toward, become the big aha.

[25:56] Justin Venneri: Yeah, 2026 is shaping up to be a big year of change, so we're excited for that. So, Jim, thank you very much for joining us on the show. Look forward to staying in touch and I hope to have you back on. Maybe we can make this an annual thing.

[26:07] Jim Winkler: Appreciate it, Justin. Thanks.

Want to stay apprised of the latest Judi Health news? Sign up for our monthly newsletter!

Interested in transitioning to an aligned and transparent pharmacy and health benefit partner? Click here to get in touch with our team!

Disclaimer

This podcast is for informational and entertainment purposes only. The views expressed are those of our guests, do not constitute professional advice, and may not represent Judi Health's/Capital Rx's position on any matters discussed. We make no representations or warranties regarding the accuracy or completeness of the content; information is subject to change and may not be updated.

.webp)